clear

All your underwriting questions answered..

Income Protection (IP) tax notices for FY24-25 will be issued from mid-July to mid-August.

The cost of breast and ovarian cancer in Australia (private vs public health system).

Help your clients get on the right track to a healthier, longer, better, life.

No email card details from 13 June. Find out more.

In our last Adviser News edition, we launched Ask Us, where we take your top questions on a topic and answer them.

Help your clients avoid the Medicare Levy Surcharge, and review Lifetime Health Cover loading to reduce premiums.

Discover the 5 Ds - Dates, Duration, Diagnosis, Drugs, Details – for smarter risk profiling. Want to know how?

During May AIA Health clients can receive 4 weeks of free premiums and have 2 weeks of premiums donated to MDC.

We've launched our new Product Disclosure Statement with simplified definitions that better support your clients.

Mother’s Day Classic, Australia’s cherished national event, returns in 2025 to fund life-saving breast and ovarian cancer research.

AIA Australia was proud to be the key partner for the FAAA Sydney Metro Community INSPIRE International Women’s Day Lunch.

Diversify your income and expand your client base with AIA’s OVHC Referral Program.

Discover how life insurance supports clients across life stages despite the challenges.

Cost of living pressures are on the rise. Get some tips to help your clients retain cover and protect their future.

See how Jim regained mobility, confidence and his CEO role after a hip replacement and unexpected complications.

Beat the health insurance rate rise! Help clients lock in 2025 premiums by reviewing policies in February and March.

On 15 December 2024, AIA released a new PDS to reflect recent changes.

From CEO to an accident that would change his life, read how Brad, is pushing forward to a plan to return to work.

In 2025 we're giving AIA Vitality members more ways to earn points.s. We're also making changes to the AIA Vitality fee.

With 1 in 5 Australians experiencing mental illness in any year, help your clients access psychologists at a reduced rate.

After a serious physical assault at work, Michael had a long recovery ahead. Read how rehabilitation support helped.

Did you know, on average, your clients' forms are processed 9 days quicker when using DocuSign?

Do you have clients impacted by the recent premium increase who don't have AIA Vitality?

Here’s some helpful information to help discuss private health insurance with clients.

Meet Will, a 48-year-old Landscaper who, after suffering a lower back injury was unable to work. See how rehabilitation helped Will.

In the first six months of the reward, we've seen great early success. Help more clients reach this milestone.

Alter existing TPD Maximiser and Income Protection Super Extras benefits without completing a Cancel & Replace application.

We’re making changes to when we will accept AIA Priority Protection Cancel Replace applications without full underwriting.

The current economic conditions can be challenging for clients. So we've created a resource to help manage these challenges.

Our 2023 claims data outlines the average age of claimants. Could this help your next client discussions?

Did you know that our new Adviser Portal offers enhanced reporting capabilities to help support your client conversation?

Effective 4 November 2024, the policy fee for inforce and new business will be increasing.

See how Ben reached out to AIA and got the support he needed after an injury.

Like life insurance, regular reviews can help ensure they have the right cover for their needs.

Read how Sam was impacted by cancer, and through rehab was able to improve his outcome.

Had clients whose policy lapsed due to non-payment of premiums? We’ve made changes.

Have a client who wants to review an existing exclusion or non-medical loading? We’re simplifying our process.

Discover what’s new from AIA Vitality including when the Apple Watch Benefit will be returning.

Effective 29 July 2024, Resolution Life will be incorporating the remaining AIA Savings and Investments customers into their ecosystem.

As of 16 August 2024, AIA will no longer be sending financial advisers’ correspondence via post for any ex-CMLA (CommInsure) policies.

Andrew was impacted by depression and anxiety, but with the help of our rehabilitation services, is returning to things he enjoys.

1 in 3 Australians feel lonely. The good news is, helping end loneliness doesn’t need to be complicated or costly.

With the April launch of AIA Vitality Silver Status reward, we’re seeing increased early engagement by new AIA Vitality members.

As of August 2024, changes are coming in how we accept Credit Card details.

Exclusive access to benefits and rewards for your AIA Priority Protection clients with annual premiums over $12,000.

We are pleased to confirm that Income Protection (IP) Tax Notices for the 2023-2024 financial year will be issued to your clients from mid-July.

See how a client reached AIA Vitality Silver Status within 24 hours and received a $500 member reward, as well as the Adviser.

In our continued commitment to become more digital, we’ve made further updates to how we communicate with your clients.

Would your clients benefit from our rehabilitation services?

Is enough focus being placed on the insurance needs of women?

Due to Go Bookings exit from the Australian market, we're making changes to how you book in tele-interviews and health consults.

Help your clients get to AIA Vitality Silver Status within the first six months of their membership and get rewarded. T&Cs apply.

Wrap up of our recent Adviser Summit event held across 5 major cities. Find out what was discussed and what’s coming.

Rehabilitation services can play a crucial role in getting claimants back to wellness. See how Sally benefitted from rehabilitation.

See how Paula benefited with the support of your Rehabilitation Service when she was impacted by mental health.

Discover how our Menopause Program could support your clients to live healthier in this transitional phase.

We know nutrition plays a huge part in overall health. What if we could support clients with their diet and help earn AIA Vitality points, too?

When it comes to claim time, a clients biggest asset may be themselves. Our rehabilitation service gives clients more options.

We’re excited to give our members the opportunity to earn the latest Apple Watch Series 9 (GPS) 41mm through our Apple Watch Benefit.

We've launched a new digital experience aimed at providing support and guidance as clients approach their policy anniversary.

While scams are not new, the digital age has seen scams reach another level. Get some tips on what to look our for with some key red flags.

Last month we highlighted Anne’s rehab story, this month let’s see how Diane benefitted from her rehabilitation support.

Striving for success and commitment to the industry led us to winning at the recent SMSF Awards night.

In 2022, we paid out over $2.1 billion in claims. Find out what our top 5 claim cases by type were.

We recently won the Roy Morgan Award for Customer Satisfaction – Major Risk and Life Insurer of the Year.

The Ovarian Cancer Research Foundation, in partnership with AIA Australia, has launched Club 1054- helping fund ovarian cancer research.

Research shows that benefits of returning to work for a client’s health and wellbeing. See how Anne was able to return to work and health.

Our latest enhancements are designed to drive efficiencies within the life risk advice process and improve pricing competitiveness.

Give your clients with annual premiums over $12,000 access to exclusive benefits and rewards with AIA Vitality.

AIA has been supporting clients experiencing Chronic Pain through our Pain Coach Program since 2018.

We’re partnering with the Future2 Foundation, supporting their 2023 Hiking Challenge, and inviting Advisers to join the cause.

When your clients have AIA Vitality, they can enjoy a taste of Platinum AIA Vitality Status.

We are honoured to win the ANZIIF Life Insurance Company of the Year Award for 2023.

We're reducing our environmental impact by switching retail notices from mail to email. What do your clients need to know?

Press pause on rate increases with AIA’s IP CORE 5-year rate guarantee when taking out a 5- or 2- year benefit period.

Help clients get 7 weeks free health insurance, plus win part of $60,000 in Virgin Australia flight vouchers when they join AIA Health by 14 September.

Introducing Olivia Sarah-Le Lacheur, AIA Australia acting Chief Customer Experience and Operations Officer, who aims to deliver better efficiencies for advisers, their staff and clients.

While common knowledge that having private health insurance has tax incentives, are client conversations making the most of this?

While claiming a deduction for personal super contributions can be a straightforward process, it is important that critical administrative requirements are not inadvertently overlooked.

.With the underinsurance gap still an issue in Australia, what objections do clients have to obtaining insurance?

View our table outlining the formula to calculate the tax-deductible premiums for your client’s income protection policies.

When is the right time to close a bank account after a client closes down their SMSF?

Have any of your clients experienced a change to their lives that might require a review of cover?

Did you know you may be missing out on seeing our AIA Vitality and AIA Healthier Life Rewards discounts on the OmniLife quoting platform?

Life isn’t straightforward – plans change! So why not future proof your clients’ options with AIA’s Forward Underwriting benefit (FUB).

As with a life insurance policy, clients should regularly review their health insurance and what their needs are. Read more about some of the key things to look out for.

First launched in 1987, the ‘World No Tobacco Day’ has helped raise awareness of the impact’s of tobacco use.

As part of our commitment to reduce our impact on the environment and improve the customer experience, AIA is going green by using less paper and communicating more via email.

If you could give your clients more control over their policy, would they benefit?

Rewarding clients for healthier life choices. Now your clients can get greater ongoing* discounts. This feature complements AIA Vitality and rewards healthier life choices, like being within a healthy weight range and being a non-smoker.

Often swayed by the ‘headline’ 15% upfront rebate under the Risk-Only option when paid via rollover, this article weighs up insurance on Platform vs Risk-Only.

There’s quite a focus on premium disclosure in the life insurance industry at the moment. To help clients better understand their cover, we’ve developed various flyers to help.

Who would have thought that when the first smartphone was released, we’d be using it to improve our health and save lives? Can a watch, smartphone and AIA Vitality be a winning formula for your clients’ health?

Last month we talked about some of the benefits for your clients in taking out private health insurance. This month we’re discussing AIA Vitality and the benefits and rewards clients get with AIA Health.

With cost-of-living pressures mounting, there is an ever-present risk that a client’s self-owned legacy or grandfathered income protection cover will be sacrificed, exposing them to potential financial strain.

Each month we’ll be talking to you about who AIA Health is, why private health insurance is important for your clients, and provide more information about the industry in general

March is Melanoma March month, and as one of Australia’s most prevalent cancers, knowing the risks, how to manage the risks and protect yourself are of great importance.

Help Aussie kids lead healthier, longer, betters lives with the AIA Healthiest Schools program. Find out some ways you can spread the word and how schools that enter the challenge can go in the running to win up to $100,000 worth of prizes

AIA Vitality members can now earn up to 7,000 AIA Vitality Points from underwriting medical checks completed when applying for their insurance cover – it’s the All or Somethings giving them a fast start to earning rewards!

In continuing to balance premiums and claims, we have recently reviewed our in-force Priority Protection premium rates.

If your client joins AIA Health on an eligible policy in September, they’ll receive $250 back for each premium paying adult (maximum $500).

If you have clients who had previously paid their Priority Protection policy with Sunsuper or QSuper, they may need to provide a new rollover authority form.

A recent review of our Initial Claims forms has resulted to improvements to our Income Protection and Total and Permanent Disablement forms.

The Priority Protection policy fee will increase in line with the Consumer Price Index (CPI) effective 1 October 2022.

With the new financial year underway, now is a good time to talk to clients about their contributions to help reduce tax and/or increase savings.

With the cost of living increasing, is it worth considering benefit indexation to help keep pace with the rising costs?

To support our vision to make Australia one of the healthiest nations in the world, we introduce AIA Embrace, a wellbeing ecosystem to help your clients thrive.

At AIA Health, we're always reviewing our products and searching for ways to deliver more value to our members. Read what we’ve done this year and the September rates.

We are currently working on improving the Adviser portal through research with advisers who have registered to help. Find out what we’ve learnt so far.

We understand the importance and value of New Business, and we are looking at ways to make it Simpler, Faster, More Connected!

With mental health impacting many Australians, AIA Australia has put in place services that clients can access. See how our Rehabilitation team helped a client through a difficult period.

As part of our new Priority Protection PDS, released on 14 August 2022, AIA presents our 5-year rate guarantee*, delivering more certainty for our Priority Protection customers.

Did you know that on average, the turnaround time for forms to be submitted via DocuSign is 9 days earlier compared to non-DocuSign methods of submission?

We are pleased to confirm that Income Protection (IP) Tax Notices for the 2021/22 financial year will soon be issued to your clients.

We all know the dangers of prolonged sun exposure. Medix reveals some of the more unfamiliar factors linked to skin cancer.

Overtime, the finer details of a client’s policy may be forgotten or misunderstood. That’s why we’ve created digital flyers to help your clients understand how their cover and premium works.

AIA Australia has released a calculator that will help advisers quantify the cost of client’s housing insurance inside superannuation and the implications on their projected retirement savings.

At the recent ALUCA Awards in Sydney, AIA Australia achieved some great results, highlighting our passion for delivering the best outcomes for our valued clients, advisers and partners.

BT Panorama and AIA Australia (AIAA) have recently partnered together, and you can now access the benefits of insurance on platform for your clients with AIAA.

From 1 October 2021, SMSFs were required to be SuperStream compliant to accept employer contributions and to send or receive member balances as a rollover.

New Silver Plus Hospital Secure product and updates to Dependant Age and Ambulance Cover extension.

You may have clients who qualify for the Loyalty Bonus which automatically increases payment by five percent at no extra cost.

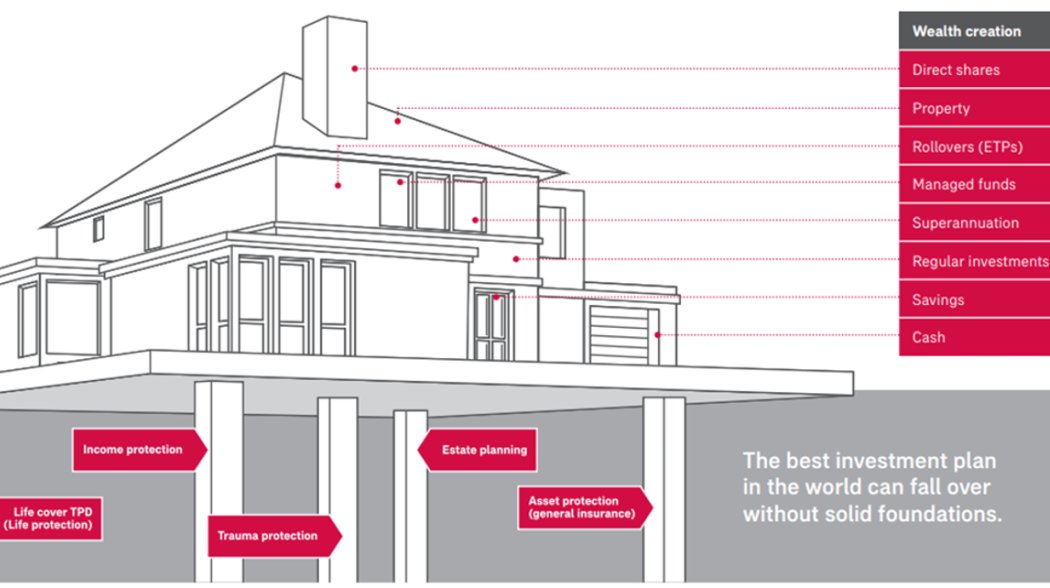

The best investment plan can fall over without a solid foundation. That’s why it’s important to balance wealth creation plans with wealth protection strategies.

AIA Australia recently launched the All or Something campaign which encourages Australians to move away from an ‘All or Nothing’ approach when it comes to their physical and mental health.

AIA Australia (AIAA) are removing the frequency loading and enabling the daily pro-rata refund for cancellations of Priority Protection policies.

Who ever thinks they will be making a claim on their Life insurance policy? The people on our list didn’t; luckily, they made the decision to apply for a life insurance policy.

We’ve made some changes to our Priority Protection PDS which include our NEW Income Replacement Tiering plus highlighting the additional support clients get with us.

Find out how the AIA Vitality Apple Watch Benefit is continuing to help our health and life customers as we step out of the pandemic.

While the ex-CommInsure products Tailored Protection are closed for new business, we are still open to make changes to existing policies.

Did you know that ex-CommInsure Tailored Protection, Total Care Plan Super and SMSF Plan policies have an inbuilt Buy Back Benefit, at no extra cost?

Predicting mental health and what causes it has been a complex task for doctors to understand. So, can it be predicted?

With the cost of living increasing and the prospect of further interest rate hikes, a more cost-effective premium on the income protection (IP) policy may be warranted for clients.

Ryan SAVED $637 per annum on his premiums after he took out $150,000 of Crisis Recovery cover combined with $150,000 of Crisis Extension cover, rather than a straight $300,000 of Crisis Recovery.

Welcome news for clients and advisers as APRA suspends IDII contract terms for at least two years.

In light of the Treasury releasing an issue paper for consultation as the first step of the Quality of Advice review, we want your input.

Everyone could do with a hand getting back on track after a challenging couple of years so we’re delaying premium increases for AIA Health and putting money back in pockets.

When disaster strikes, we look for ways to make tough times a little easier – and support those who’ve helped those in need.

AIA Australia’s lump sum income replacement calculator.

AIA Australia may have some options for your clients to help provide some peace of mind.

Another year, and based on adviser feedback, another successful event.

These templates could be helpful when constructing an SOA.

From 1 July 2022, AIA Health members who hold a Basic or a Basic Plus Hospital product will be moved from AIA Vitality to AIA Vitality Starter.

Find out how DocuSign works, helping clients and advisers save time.

Have you considered checking in with clients to see how their superannuation contributions are tracking and consider what opportunities remain for them in 2021/22?

What reforms from 2021 remain in proposal and what could affect them becoming law?

Through our AIA One Billion initiative, we aim to engage a billion people to live Healthier, Longer, Better Lives by 2030.

Over the past years, COVID-19 has presented challenges to every industry globally. There’s been short-term impacts to individuals and businesses, and we are still yet to see and fully understand what the long-term effect of the pandemic will be.

See how your clients could take advantage of AIA Health’s new offer if they join by 31 March 2022.

Find out how our 2+2 IP strategy can help your clients who are on claim for longer than two years.

Due to the ongoing spike in COVID cases, the opening hours of our retail contact centre will temporarily change from 31 January to 9am to 5pm AEDT (previously 8am to 6pm).

The insurance industry has seen changes to income protection products addressing the importance of sustainability so that when clients need their cover, it’s there.

?qlt=85&ts=1675925970069&dpr=off)