In scenario 1 – Ryan is diagnosed with a cancer that evolves.

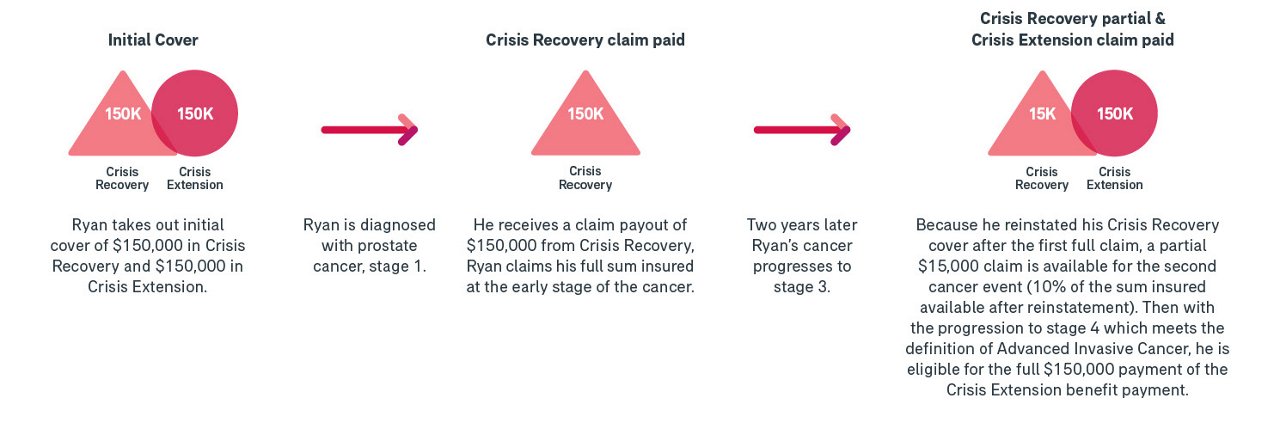

As shown above Ryan takes out initial cover of $150,000 in Crisis Recovery and $150,000 in Crisis Extension.

Ryan is diagnosed with prostate cancer, stage 1.

Crisis Recovery claim paid

He receives a claim pay-out of $150,000 from Crisis Recovery as a result of Ryan claiming his total $150,000 sum insured at the early stage (stage 1) of the cancer.

Two years later, Ryan’s cancer recurs, spreading to other parts of his body.

Because he reinstated his Crisis Recovery cover after the first full claim, a partial $15,000 claim is available for the second cancer event (10% of sum insured available after reinstatement.). Then with the progression to stage 4 which meets the definition of Advanced Invasive Cancer, he is eligible for the full $150,000 payment of the Crisis Extension benefit payment.

Without Crisis Extension, Ryan would have received a Crisis Recovery benefit for the Stage 1 cancer diagnosis, but only a partial benefit when the cancer recurred, leaving him financially vulnerable at a time when he couldn’t afford it to be. Alternatively, if he had taken $300K of Crisis Recovery, his premium would have been around 14% more expensive. (The above quote $1,364.96 vs $1,585.98, Crisis Recovery Stand Alone $1,496.88 and Crisis Reinstatement $89.10, Quote as at 13 July 2021).

If you would like to learn more about our Crisis Extension benefit, download our Technical and Position flyer, or reach out to your AIA Client Development Manager or Associate.