Take out an eligible policy by 31 July 2025 and you’ll get up to $600 cashback over your first 2 years. *On eligible products. T&Cs apply.

New member offer!

Get up to $600 cashback when you join AIA Health by 31 July*.

Get health cover with a difference

Enjoy member benefits, discounts and rewards

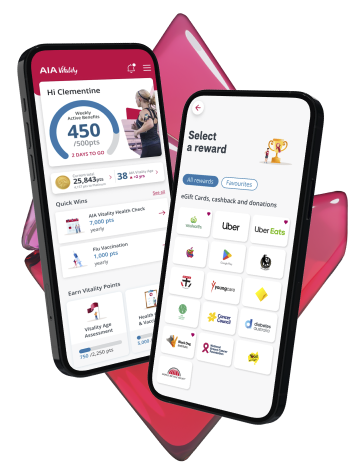

All AIA Health policies come with AIA Vitality, our science-backed health and wellbeing program which supports you to make healthier lifestyle choices by rewarding you for understanding and engaging with your health.

You can also get

^Award winning health insurance that protects and rewards.

Here is some recognition we are proud of:

ProductReview.com.au

Best Health Insurance Provider 2022, 2023, 2024 and 2025.

Rated 4.8/5*

Rated 4.9/5*

^WeMoney Insurance Awards

Digital Health Insurer of the Year 2024

Outstanding Customer Service (Health Insurance) 2024

Health Insurer of the Year 2022

Best for Quality (Health Insurance) 2022

Mozo People Choice Awards for Health Insurance

Value for Money 2024

Best Sign-Up Experience 2024

*as at August 2024

Get more from your health insurance

15-40% off dental treatments

Members who have an Extras product with

dental cover will save 15-40% off all dental treatments performed by a smile.com.au

dental cover will save 15-40% off all dental treatments performed by a smile.com.au

dentist.

Optical savings

We’ve partnered with Australia’s largest

optical retailers to give our members access

to discounted products and services.

Cancer Coach program

All AIA health hospital and combined products include access to CancerAid’s Cancer Coach program. Designed by oncologists to empower people during their cancer care journey at no extra cost.

Finding the right cover comes down to what you need

At AIA Health, we strive to simplify insurance while giving you the ability to tailor your policy. Customise your cover and maximise the benefits so you can spend more time doing the things that matter most to you.

We will help you find the right cover

Useful links

Learn more about Health Insurance

What is Health Insurance?

Hospital cover helps to cover the cost of treatment you receive in hospital. Each level of AIA Health Insurance Hospital Cover (from Basic to Gold) is differentiated by the list of treatments that are included. For example, cover to be treated in a Private Hospital for pregnancy is only available on our Silver Plus Family Hospital and Gold Hospital cover.

Hospital cover helps to cover the costs of being treated in hospital. Having Hospital cover means you can be treated in a private hospital and avoid public hospital waiting lists. You get more control over where you're treated, and who treats you.

Extras cover is for treatments that do not take place in a hospital, like visits to the dentist, physiotherapy or optical services. AIA Health Insurance Extras cover can only be taken with Hospital cover. The types of services you can claim under your Extras cover will depend on the level of cover you take out, but essentially this type of cover is to help with services and treatments received out-of-hospital, that aren't covered by Medicare.

Combined cover is when you take out both Hospital and Extras cover. That's why you'll hear the term 'Hospital and Extras' thrown around so much when it comes to health insurance - it's a popular choice.

Most Australians with private health insurance currently receive a rebate from the Australian Government to help cover the cost of their premiums, either as:

- A reduction of your AIA Health Insurance premium; or

- A lump sum payment when lodging your tax return.

The level of your rebate depends on your income and your age. To find out more and to find out how much you could get back head to the Private Health Insurance Rebate Calculator on the Australian Taxation Office website.

The MLS is simply an extra tax that people above a certain income threshold have to pay if they don't have eligible private hospital cover. It's calculated in three tiers for singles and couples/families. You can find out more about that here.

The Lifetime Health Cover (LHC) loading is a Government loading on your private hospital cover premiums. It was introduced on 1 July 2000, to encourage people to take out private hospital cover earlier in life and encourage them to maintain it. LHC is a 2% loading on top of your premium for every year you don't have hospital cover after you turn 30. The maximum loading is 70%. You can find out more here.

A waiting period is the time between joining or upgrading your level of cover and the date from which you're allowed to start claiming. Waiting periods exist for all services within both hospital and extras covers and apply to:

- New memberships

- Additional members to a membership (unless the new member/s has/have previously served all waiting periods on equivalent cover with AIA Health or another fund) except for newborns, adopted and permanent foster children where the family membership has been in existence for at least two months

- Existing members who upgrade their cover to a higher level of cover

- Members who transfer to AIA Health Insurance from another fund to a higher level of cover than that of their previous fund

- Treatment for a pre-existing condition.

Waiting periods for Hospital treatment range from one day to 12 months.

- There is a one day waiting period for ambulance cover and treatment resulting from an accident

- A 12 month waiting period for pregnancy

- A 12 month waiting period for pre-existing ailment, illness or condition (except for psychiatric, rehabilitation and palliative care)

- A two month waiting period for any other hospital treatment.

Waiting periods for Extras treatments vary by the treatments vary from two to 12 months, depending on the type of service. These are listed below:

- General Dental - two months

- Preventative Dental - two months

- Major Dental - 12 months

- Orthodontics - 12 months

- Optical - six months

- Physiotherapy – two months

- Hydrotherapy - two months

- Myotherapy - two months

- Exercise Physiology - two months

- Chiropractic - two months

- Osteopathy - two months

- Naturopathy - two months

- Homeopathy - two months

- Acupuncture - two months

- Remedial massage - two months

- Podiatry - two months

- PBS Pharmacy - two months

- Psychology - two months

- Audiology - two months

- Eye therapy - two months

- Speech therapy - two months

- Antenatal and postnatal - two months

- Occupational therapy - two months

- Medically Prescribed Appliances (incl. hearing aids) - 12 months

- Orthopaedic appliances - two months

- Swimming lessons - two months

- Dietetics - two months

- Other including: Bowel cancer identification kits (one every two years), Melanoma Surveillance Photography (one per year) - two months.

We have agreements with hundreds of private hospitals and day surgeries in Australia - that's what we're talking about when we say participating private hospital. To find out whether your hospital is a participating one call us on 1800 333 004. If you're admitted to a private hospital that's not on our list you may have to pay higher out-of-pocket fees.

AIA Health Insurance is a member of the Australian Health Services Alliance (AHSA). A non-agreement hospital is a hospital that has not signed an agreement with the AHSA. If you receive treatment from one of these you may incur large out-of-pocket expenses. Call us on 1800 333 004 or email us at health.memberservices@AIA.com.au to find out if the hospital you want to be treated at is a participating hospital so you can avoid these costs.

A pre-existing condition is a condition - assessed by one of our medical practitioners - that you've had or shown symptoms of having within the past six months before you joined us, or changed your cover. This affects your cover quite a bit, and there's more on this in our member guide.

The Federal Government sets a schedule of fees for eligible services provided by doctors to inpatients in hospital. Medicare pays 75% of these fees and health funds like AIA Health Insurance pay the remaining 25%. Doctors and providers are not restricted to charging this fee and are able to set their own fees, which can be higher than the scheduled fees. If your doctor chooses to charge a higher fee, there will be a gap between what the doctor charges and what the Government and AIA Health Insurance will pay. This is the 'Gap' and can leave you with significant out-of-pocket expenses. If your doctor participates in AIA Health's Access Gap Cover, we'll pay more than the 25% of the schedule fee - leaving you with drastically reduced, or even eliminated out-of-pocket expenses. The best way to find out if your doctor is registered for Access Gap Cover is to ask them.

AIA Health Insurance covers you for all clinically necessary ambulance services for emergencies in Australia. Emergencies are circumstances when immediate hospital treatment is required for a serious and acute injury or condition where the viability or function of an organ or body part is threatened. Check with your state Ambulance authority to ensure you have the right level of cover for non-emergency ambulance transport within Australia.

A Private Health Information Statement (PHIS) is a summary of the key product features of your cover. You will receive a link to download a copy of your PHIS when you join AIA Health Insurance and it is available to download from our Online Member Services portal.

- Click on 'Member Login' on the website header.

- Log into the member portal.

- Select 'Correspondence' from the left hand side menu.

- Underneath this, select 'All Correspondence'.

- Under 'Subject Area', click on [+] next to 'General Messages'.

- Scroll down to the earliest message, find the message titled "Welcome to AIA Health Insurance".

- Under 'View', find links to view/download your Private Health Information Statement and relevant policy fact sheet.

If you have less than 12 months membership on your current hospital cover, you’ll need to contact us by phone on 1800 333 004 or by email at health.memberservices@AIA.com.au before being admitted so we can determine whether the waiting period for pre-existing conditions applies.

It can take up to five working days to complete this assessment, so make sure you factor this in when you book your stay. If you go ahead with your admission without confirming your entitlements and we subsequently determine your condition to be pre-existing, you’ll have to pay all outstanding hospital and medical charges not covered by Medicare.

The best way to find out is to ask them. Every doctor is different and some will even opt in or out on a patient-by-patient basis. If your doctor participates in AIA Health Insurance's Access Gap Cover they can either choose to participate as a no gap charge or a known gap as follows;

- No Gap’: Your doctor participates in Access Gap Cover and charges you no out-of-pocket for the treatment you received as an inpatient, or

- ‘Known Gap’: Your doctor participates in Access Gap Cover and charges you a reduced out-of-pocket fee for the treatment you've received as an inpatient. You will be aware of the costs before surgery.

Just remember to check with your doctor before agreeing to any treatment.

Members with extras cover with dental are eligible to save between 15-40% off dental treatments performed by a smile.com.au approved dentist. Read more.

No. AIA Vitality is a science-backed program that helps you learn about your health, improve it and stay motivated with rewards. Find out more.

We've got the basics covered above. For anything we haven't covered, head to privatehealth.gov.au

This one's on us. All you need to do is give us the details of your current insurer and we'll take care of the rest.

Your cover starts as soon as we receive your first payment and you can begin claiming as soon as any applicable waiting periods are over.

You can amend your details at any time by logging in to the Online Member Services portal and editing your AIA Health Insurance profile. Alternatively, you can give us a call on 1800 333 004. This goes for changing your address details, payment details or if you change your name when you get married.

Only the member - the person whose name the policy is under - and anyone the member authorises can make changes to your cover.

We recommend you contact us prior to your admission to find out if the hospital you are to be admitted to is on our participating hospital list and to confirm that you have the right level of cover for the treatment you are seeking. If the hospital you are admitted to isn’t one of our participating hospitals, you may not be covered in full for your accommodation or theatre costs. Contacting us first means you will know what types of benefits you will receive and what your out-of of-pocket costs will be.

When you are admitted to hospital, the hospital will ask if you have private health insurance and will check your eligibility with us. All AIA Health Insurance hospital covers includes an excess cost to help lower your premium and you will be asked to pay the excess when you are admitted to hospital.

You can choose to pay via direct credit with a credit card or direct debit via your bank. Each method and its benefits are detailed in our member guide. Payment cycles are weekly, monthly or annually. Please call us on 1800 333 004 if you want to change how you pay your premium.

If you’re planning to start or grow your family and your hospital cover doesn’t include pregnancy, you’ll have to upgrade your cover at least 12 months before giving birth to ensure all waiting periods have been served. Newborn babies aren’t admitted as patients in hospitals unless there are complications or your baby requires medical attention. In these instances your baby will be covered provided they are added to the policy. Give us a call to add a baby to your policy.

If your card is lost or stolen you should contact us as soon as possible to avoid fraudulent claims and we'll send you a brand new one. Remember, whenever you get a new card from us, your old one automatically becomes invalid so throw it away to avoid any confusion.

An excess is an upfront payment that you are required to make when submitting a hospital claim. A higher excess will reduce your premium. A lower excess means you’ll pay less on admission to hospital, but your premium will be higher. Some AIA Health Insurance products offer you a choice of excess options, either $500 or $750 for an individual. The excess applies to the policyholder (and partner where applicable) once per person, per calendar year. Child dependants covered on a family policy are not required to pay an excess.

Where your policy includes an Excess Refund, it means that if you hold this policy or another eligible policy for at least six months and hold Silver AIA Vitality status or higher, AIA Health Insurance will refund 100% of your hospital excess.

You will need to pay your excess when you’re admitted to hospital and then you can claim this amount back. See your member guide for more details.

To qualify for benefit payments, these must be custom-made by practitioner podiatrist or orthotist. For an orthosis to be custom made, a plaster cast or mould must be taken. Please note that customising, heat moulding, trimming or adjusting an existing ‘off the shelf’ appliance does not constitute a custom-made appliance. Orthopaedic appliances attract benefits where the application of which has resulted from, and is required immediately following, the injury or surgery, and a doctor's letter of recommendation is required prior to claiming.

AIA Health Insurance does not pay benefits for the hire of any health appliance or equipment. We will, however, fund a percentage of the purchase of the following appliances up to your annual limits, providing you lodge a doctor’s letter of recommendation with your claim:

- Blood glucose monitor

- Extremity pump

- Nebuliser pump

- Sleep apnoea monitor

- Pressure garments

- AIA Health Insurance approved orthopaedic appliances

- Non-surgical prostheses

- Tens monitor.

A benefit replacement rule applies to some items/services covered by AIA Health Insurance’s extras cover. This means that after you claim for an item, you must wait a specified period before you can lodge another claim for the same type of item. Call our Member Service Team on 1800 333 004 to find out which treatments have benefit replacement periods.

You can claim for weight loss programs under our Dietetics Extras cover but only when it has been recommended, in writing, by a doctor for preventing or improving a specific health condition. Also, the weight loss provider must be a member of the Weight Management Council of Australia and agree to abide by the Weight Management Code of Practice.

Here are some well-known providers that we’re happy to approve:

- Weight Watchers Australia

- Jenny Craig Weight Loss Centres Pty Ltd

- Simplicity Weight Loss

Please note that we only cover weight loss program fees and will not provide any benefits for meals, groceries or exercise components.

You can only claim extras benefits where treatment is received in person from a recognised health practitioner, received in Australia. To find out if your practitioner is recognised you can ask your practitioner before you make your appointment or call us on 1800 333 004 (we’re open from 8am to 6pm AEST). You cannot claim for treatments you provide to yourself or to members of our family or business partners and members of their family.

Yes - but only when purchased online from Australian optical and pharmaceutical providers when a script is provided. For a company to be considered an Australian provider, an ABN needs to be visible on the company’s website. Benefits for services, treatments and other costs received overseas are excluded and will not receive any benefit.

Family cover provides cover for the member, their partner and their children including dependant students up to the age of 25. Cover for child dependants ceases once they turn 21, unless they qualify to remain on the policy as a student dependant. When a child dependant turns 21, they have two months to get their own cover and not have to serve any waiting periods if moving to equivalent or lower cover. Student dependants also have two months from either turning 25 or ceasing to be a student to get their own cover. For mid-year school, apprenticeship and traineeship leavers who transfer from their parent’s AIA Health Insurance policy within two months of leaving school or finishing an eligible apprenticeship or traineeship through a registered training group will not have to serve waiting periods if they transfer to an equivalent or lower level of cover. A letter from their school or registered training group confirming the date of completion is required. For end of year school, apprenticeship and traineeship leavers, they are covered until 31 March of the following year and will not have to serve waiting periods if they transfer to an equivalent or lower level of cover.

You can only claim on Extras treatments that are specifically included in your cover. Here’s a list of some of the treatments (not all) that aren’t covered:

General

- Services or treatment for which anyone covered has a right to claim damages or compensation from any other person or body

- Treatment where the member and/or dependant is eligible for free treatment under any Commonwealth or State Government Act

- Services or treatment rendered more than two years prior to the date of claiming

- Services or treatment not covered by your membership and/or is rendered while the membership is in arrears or is suspended

- Services or treatment rendered by a practitioner not in private practice and/ or not recognised by bodies approved by AIA Health Insurance.

Pharmacy

- Contraceptive, fertility and IVF drugs available through the Pharmaceutical Benefits Scheme (PBS)

- Food supplements

- Pharmacy items, where they are available over the counter and purchased with or without prescription

- Drugs purchased overseas

- Mass immunisation, services rendered in the course of the carrying out of a mass immunisation

Pharmaceuticals that are not considered an S4 or S8 drug.

Dental

- Dental procedures where a limit on the number you can have has been exceeded

- Dental procedures unless tooth Identifications (ID) are supplied by the provider

- Dental procedures carried out and charged by a dental mechanic, other than an advanced dental technician

- A range of dental procedures when provided on the same day for example a filling on a tooth that has been removed. Please contact us for further information relating to these exclusions

- A benefit will only be paid for a single crown per tooth every five years.

Foot orthotics

- Any procedure provided by a physiotherapist or chiropractor.

Orthopaedic appliances

- AIA Health Insurance specified and approved orthopaedic appliances purchased for support purposes only.

Pressure garments

- Pressure garments purchased for reasons other than the treatment of burns, varicose veins, lymphedema or post-operative surgery up to 60 days from hospital discharge only.

For more information please see our member guide.

When you join us you'll receive a full welcome pack with all you need to make the most of your cover. If you can't see what you're looking for above, take a look at our member guide or call us on 1800 333 004.

Where your policy includes a travel and accommodation benefit this can be used to claim towards the travel and accommodation costs of either yourself or a carer (if applicable) for a hospital admission.

Benefits are only eligible where the round trip is at least 200km within Australia. Benefits are capped at $50 per day for accommodation and 15 cents/km for travel for you and your carer.

There are lots of ways to make a claim. You'll just need to make sure you've served all your waiting periods before you start the claims process. Then, if you have Extras cover, you can simply use your membership card. Alternatively, you can use our member portal, or even claim by post. We've detailed the ins and outs in the member guide (plus some extra process info that may come in handy).

You can see them all online. Simply log in to our member portal and head to the Claims section to look at your history.

It doesn’t happen often, but there are instances where benefits are not paid at all or are paid at a lower level. These are when:

- The treatment is not covered under your policy

- The treatment was not provided by a recognised provider

- The treatment was not provided in Australia

- You’ve already claimed the maximum allowable benefits during a specified period

- You’ve transferred to AIA Health Insurance from another fund and have already claimed for that treatment

- It’s been more than two years since the treatment you’re claiming for

- The health care account has been incorrectly itemised

- You have an excess to pay on your chosen level of cover

- The service is subject to a waiting period or another limit

- You’re claiming for treatments carried out overseas

- Treatment was provided to or from a family member or business associate

- If AIA Health Insurance believes that you are not receiving acute care after 35 days of continual hospitalisation

- Surgery is performed in hospital by a registered podiatrist/podiatric surgeon

- When no MBS item number is provided by the health practitioner

- If the MBS item is being performed for a cosmetic reason and not medical

- The treatment was the second treatment performed on you in a day by a single practitioner.

To find out more, we recommend checking out your cover’s detailed terms and conditions published in our Fund Rules. These are available by calling us on 1800 333 004.

We thought you'd never ask. AIA Vitality is what makes us different. For all the details on how the program can boost your wellbeing and help you to maintain a level of good health, head to the AIA Vitality page.