On 20 February 2022, we released our new Product Disclosure Statement (PDS).

New AIA Priority Protection PDS

ARTICLE

20 February 2022

3 mins read

3 mins read

At AIA Australia (AIAA), we have a dream to make Australia the healthiest, best protected nation in the world. In order to achieve our goal, it’s the small somethings that count.

As we continue to take a leadership approach, regularly reviewing and improving our offer within the new world of Income Protection and in response to insights and ongoing adviser feedback, we’re pleased to introduce a Flat 70% income replacement ratio option within Income Protection CORE.

We are also improving the design of Income Protection CORE’s 5 year Benefit Option to a Flat 70% structure and Own Occupation definition for the duration of the claim.

By introducing these new product enhancements alongside our existing 70/60% reducing replacement ratio option you can provide more choice for clients. As we continue to support sustainability within the Income Protection market, we also recognise that in some instance’s clients may require the additional benefit support a Flat 70% option provides.

Should you have any questions, please don’t hesitate to contact your AIAA Client Development Manager or Associate.

Priority Protection Enhancements

- NEW Income Protection CORE Flat 70% income replacement ratio option.

- NEW Flat 70% income replacement ratio and Own Occupation for new 5 year Benefit Period policies.

- New Lump Sum Accommodation Benefit - reimburses accommodation costs for Immediate Family Members of up to $250 per day for a maximum of 30 days with an AIA policy cap of $7,500 per Life insured. (Not available where policy is solely inside superannuation).

- New Counselling Benefit - provide $200 for each session of grief counselling for an Immediate Family Member of the Life Insured with a registered counsellor or psychologist. (Not available where policy is solely inside superannuation).

- Premium and Cover Pause Benefit – this benefit becomes a permanent option after being offered to clients during the COVID pandemic. Customers can apply to temporarily suspend premiums and cover for three, six or 12 months, for a cumulative maximum of 12 months, in certain circumstances. Designed to provide temporary support to customers who are experiencing financial hardship. (Not available inside super or a superannuation linked policy).

Also, worth noting are underwriting changes to the Working From Home definition and the introduction of some positive pricing adjustments to our new business rates including a realignment of our bundled and lump sum bundled discounts. You’ll see these changes reflected in the quoting tools and research software.

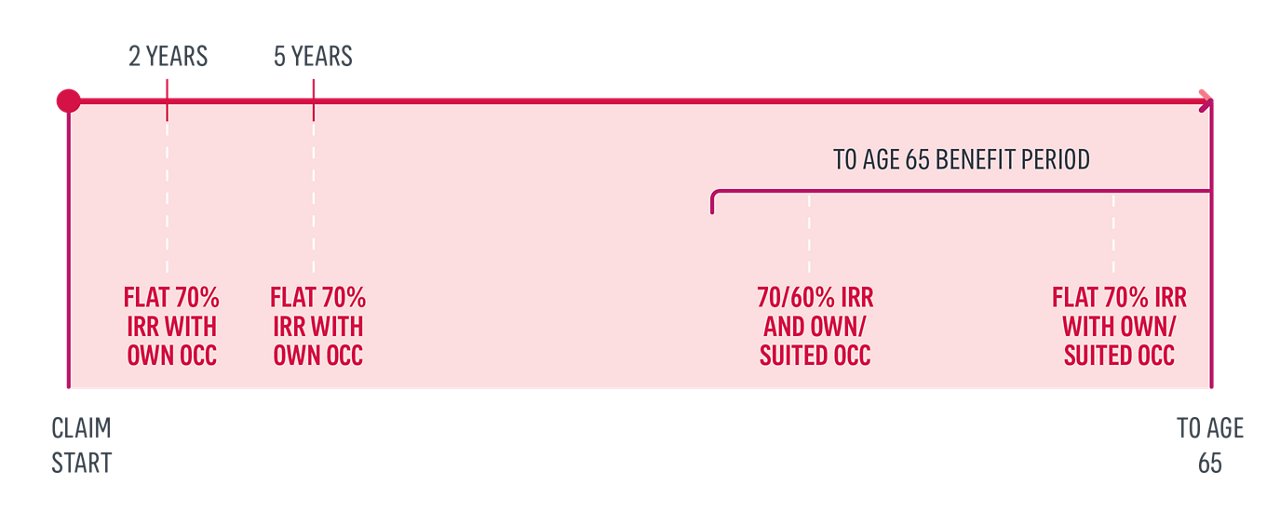

Which benefit option is right for your client?

- 2 year benefit period – Flat 70% IRR with Own Occ for duration of claim.

- 5 year benefit period – Flat 70% IRR with Own Occ for duration of claim.

- To age 65 benefit period – 70/60% IRR and Own/Suited Occ transition after 24 months.

- To age 65 benefit period – Flat 70% IRR with Own/Suited Occ transition after 24 months.

Income Protection Core includes

- Benefit Indexation

- Salary Increase Benefit

- Recurrent Disablement

- Rehabilitation Expenses Benefit

- Premium and Cover Pause - NEW Enhancement

- Complimentary Interim Accidental Income Protection Cover

- Needlestick Injury (Occupation Category M only)

- Elective Surgery

- Involuntary Unemployment Waiver of Premium

Income protection core optional benefits

Claims Escalation - allows for the claim payments to be increased each year in line with the Consumer Price Index Increase (CPI Increase).

Retirement Protector – an important addition to an advice strategy which pays a monthly benefit to a nominated Superannuation Fund when the client is either a Total or Partial Disablement Benefits. This protects the client’s retirement plans during their period of illness.

Example:

A client’s PDI is $100,000, when a claim is paid, they receive a monthly payment of $5,833 per month (70% of $100,000) into their bank account and $833 per month into their superannuation account.

A client’s PDI is $100,000, when a claim is paid, they receive a monthly payment of $5,833 per month (70% of $100,000) into their bank account and $833 per month into their superannuation account.

How are claims assessed occupationally for policies that include a switch from own occupation to suited occupation?

For the first 24 months – the monthly benefit paid is assessed against a Material and Substantial Duties definition of their Own occupation. After 24 months, the claim is assessed against a Suited occupation.

For Income Protection CORE, Own Occupation means the trade, profession or type of work the client was working in prior to the claim, whereas suited occupation means an occupation the client is reasonably suited to by education, training or experience. Remember that it is the Material and Substantial duties of their Own Occupation or Suited Occupation that they’ll be assessed for.

AIA offers programs to help clients live healthier, longer, better lives.

Priority Protection clients have access to exclusive AIA support programs including Medix and AIA Rehabilitation. These focus on helping clients to live a healthier, longer, better life either before or while on claim with us.

Supporting you with integrated advice strategies

At AIAA we’ve developed a deep understanding of the challenges and intricacies advisers face in providing advice within the new Income Protection parameters.

The recent changes to income protection highlight the importance of using a wide range of insurance products in combination within advice strategies. Our Technical team are here to support you and your teams with this transition through their specialist knowledge on the changing income protection journey and regulatory landscape.

Access our suite of support materials provided to assist you.

Where do I access the new priority protection forms and support documents?

The update introduces a new application form and other updated administrative documents, these are available to download here or from the Adviser Site.

New PDS and Application forms

Adviser support resources

For more information about AIAA’s Priority Protection contact your AIAA Client Development Manager or Associate, or our Adviser Support team on 1800 033 490.